Is Biotech Junk?

Everyone hates biotech and maybe you should too.

Image: ChatGPT, Ascendant BioCapital

When I tell asset allocators I invest in biotech, I usually get one of two reactions. The more common one is, "Oh, you do biotech? I've done a couple of biotech deals. I know a guy," which is generally followed by fifteen minutes of playing the role of therapist, listening to how spectacularly awful, capital-intensive, and costly the experience was. The rarer response is, "We love biotech; we're full up with managers and we're building out the vertical to do direct deals ourselves or scale up our co-investments."

Both responses tend to be the wrong ones. The former avoids the sector categorically, writing it off as junk. The second leans in too hard, finds that they are paying too heavily in fees to managers whose performance doesn't scale proportionately to AUM, and then decides it is straightforward enough to replicate through internal sourcing, underwriting, or co-investments.

The first reaction is why the sector has a reputation of being junk: all hopes and dreams of future benefit, requiring lots of money today to happen. And it isn't entirely unearned. Biotech dilutes relentlessly, burns cash on binary bets, and trades like a junk factor.

Beyond the disciplined underwriting of calculated risks worth taking, there is no willing away a risk that is unknowable until a specific experiment returns a result telling you, with statistical rigor, whether a hypothesis is right or wrong. No founder, CEO, engineer or salesperson can sell, code, manage or grind that risk into submission, as can be the case in other sectors.

Biotech equities deal in facts discovered in real time through the empiricism of the scientific method. The problem is that investors are still human. They can be seduced by a compelling story, a charismatic executive, or data that looks too good to be true. Too often, the latter are revealed to be experimental artifacts, or, occasionally, outright fraud: manufactured results.

Red, White and Melting: Hot Biotech Summer

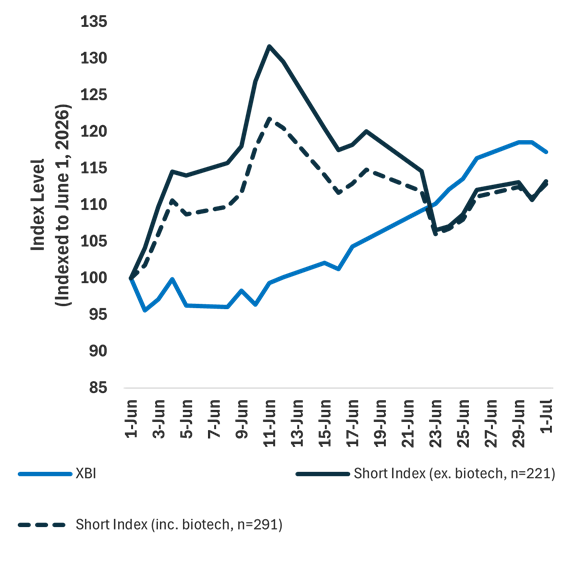

Apparently, quant strategies had their worst week since 2023 in June, driven by a "junk rally" in heavily shorted names. Unsurprisingly, biotech melted up in the same window. I was morbidly curious—how much of the strength I had observed in biotech was just forced covering by the quants? And were any biotech bears left standing?

The XBI rose 17.2% between June 1 and July 1, right alongside a 13.3% pop in a bespoke composite of the 221 most heavily shorted stocks, excluding biotech. I weighted the basket 40% by dollars short and 60% by percent of float short to capture both position size and "squeeziness" or how crowded the short is relative to the shares available to buy back. Was this proof of junkiness by association?

Looking at the daily data, I was surprised to find biotech's moves were uncorrelated with my junk index and largely opposite in sign (Figure 1). This was despite a near-heroic effort to purge the 70 biotech names from the list of the 291 largest stonks—I mean stocks—with more than 20% of their float sold short. More amusingly, adding the biotech names back actually made the index look slightly less junky, while still leaving it with daily price dynamics that were largely the mirror image of the XBI during the period.

Image: ChatGPT, Ascendant BioCapital

Figure 1: Biotech's June melt-up was uncorrelated—and oppositely signed—to the "junk" short-squeeze index

|

|

|

Source: Yahoo Finance, Ascendant BioCapital Analysis

Why Biotech is More like Nuclear Waste than Junk: Δ m = Δ E/c2

It's clear that "junk" is the wrong taxonomy for biotech. Biotech is widely understood to be uncorrelated from the rest of the market, but the source of those persistent uncorrelated returns is easy to miss, often obscured by headlines taken in isolation about a clinical trial readout or an M&A event. The recent cadence of M&A looked like the obvious candidate for biotech's nearly monotonic climb through June. But was it M&A momentum or something else? And is there more or less equity outstanding after netting the M&A vs. biotech's insatiable appetite for fresh equity?

Biotech is a chronic, compulsive issuer, conducting well over two thousand financings and raising roughly $171 billion of gross public equity since 2021 (excluding ATMs and stock-based compensation). No sector goes back to the well more often, and for a structural reason: biotech is the public market's one large cohort that is overwhelmingly pre-revenue, raising tranches of capital in a stage-gated manner against binary milestones, with the equity market as its only reliable source of gas. A clinical-stage company that cannot sell stock must partner, sell itself, or shut down. So it sells stock when it can, and then sells some more. Healthcare desks run more follow-ons, PIPEs, and registered directs than any other sector. Sort the equity universe by how often a company issues, and biotech sits at the top of the leaderboard, precisely the profile every factor model that penalizes dilution is built to punish.

But gross issuance is not net issuance. Yes, biotech prints stock relentlessly. It also has a sneaky habit of disappearing. Companies raise capital for years, then demonstrate a line of sight to a registerable drug that can deliver meaningful clinical and commercial value, and then get swallowed whole, mostly in cash acquisitions that retire their shares permanently.

Net the two effects and the result is the opposite of what nearly everyone assumes: in every full year since 2021, and again in Q1 2026, biotech has been a net retirer of public equity (Table 1). It cannot shrink through buybacks due to insufficient cash flow. It shrinks because pharma needs to and does buy. From 2021 through 2025, roughly $444 billion of cash acquired public biopharma companies against about $158 billion of public equity issuance, removing close to three dollars of stock for every dollar raised, nearly 25% more than the $2.26 removed for every dollar raised by the broad US equity market from 2021 through 2024.

Table 1: Biotech net equity issuance vs. the broad market, 2021—Q1 2026 ($ millions), parentheses denote negative issuance (net share retirement)

|

Year |

Gross Public Biotech Equity Raised |

Stock Retired via Upfront Cash M&A |

Biotech Net Issuance |

US Broad-Market Gross Public Equity Raised |

Broad-Market Net Issuance |

Biotech % of Market Net Retirement |

|

2021 |

39,277 |

(52,599) |

(13,321) |

376,400 |

(156,280) |

8.5% |

|

2022 |

19,044 |

(84,606) |

(65,562) |

86,020 |

(634,550) |

10.3% |

|

2023 |

23,342 |

(139,549) |

(116,207) |

126,800 |

(603,330) |

19.3% |

|

2024 |

42,333 |

(50,597) |

(8,264) |

201,160 |

(395,140) |

2.1% |

|

2025 |

33,843 |

(116,762) |

(82,920) |

N/A |

(309,180) |

26.8% |

|

2026 (Q1) |

13,203 |

(31,426) |

(18,223) |

N/A |

+25,200 |

mkt. flipped to net issuance |

Source: BCIQ & FactSet, as of June 23, 2026; Federal Reserve Enhanced Financial Accounts; SIFMA Capital Markets Fact Book; Ascendant BioCapital Analysis

Biotech seems like inflationary junk because the market is focused on gross issuance. It is more aptly classified as nuclear waste, behaving as a deflationary asset because it is shrinking in mass faster than the broader US equity markets for every dollar raised. Like radioactive decay, the sector constantly throws off daughter particles in the form of new financings, new companies, new ideas, new science worthy of investment. Yet each successful acquisition converts part of that mass into energy for the next cycle, leaving less public-market equity behind than before.

The Sector that Both Pharma and Equity Investors are Net Short

The Federal Reserve's accounts show net equity issuance for US nonfinancial corporates deeply negative for a decade. Shrinking supply versus steady index-fund demand has been a boon for stock market investors. Biotech's share is absurdly disproportionate: 8.5% of all net retirement in 2021, 19.3% by 2023, and 26.8% in 2025. Cumulatively this is roughly one dollar in seven—and growing—from a sector many allocators treat as a rounding error or as a lottery ticket.

From 2021 through 2025, about $158 billion of public equity flowed into the sector against roughly $444 billion of upfront acquisition cash out: $2.81 returned for every dollar of public equity raised[i]. It is worth reflecting on where all the M&A cash lands, because it is not intuitive. Private venture, over the same window, collected only about $0.81 of upfront M&A per dollar in—roughly $75 billion back on $92 billion invested—against the $2.81 the public market returned. Those $0.81 count only upfront cash M&A, so it understates venture's full return, which also could consider IPO exits and M&A milestone or equity payments. By contrast, the cash exit accrues disproportionately to the benefit public biotech investors, the corner of the equity market that is actively shrinking, doing one dollar in seven of all net US share retirement, while representing only about 1% of the US stock market capitalization[ii]. For public biotechs this works out to a net drain over $286 billion over the past five years. And much of that cash leaves forever. Some recycles into the next fund; the rest disappears into taxes, pension obligations, diversification into other sectors and strategies, or the beach houses, boats, caviar, vintage Bordeaux, and the occasional Gulfstream that mark a job well done.

In supply terms, pharma and the market are effectively net short biotech, systematically selling down claims on a sector that generates predictable compounding returns in both human health and capital gain.

Net share issuance is one of the most persistent anomalies in asset pricing. Fama and French and others find that issuers underperform and retirers outperform, robustly. But the analysis only considers the change in shares year over year for firms that remain in the sample the following year.

If you were to sort living biotechs by issuance, you would get a parade of serial diluters. The factor models would short them without considering the payoff, the exit. A biotech that raises round after round to fund development of a breakthrough new drug is a "value-destroyer," seeing volatile but attractive share price gains right up until it is acquired at a premium and vanishes from the dataset altogether as 100% of its shares are removed from the market.

As a result, biotech gets branded as a chronic issuer even though its right tail of transcendent successes—and the sector itself—behave like the market's best repurchasers.

A Buyer With a Gun to Its Head

Why would pharma keep stumping up to buy nuclear-waste biotech? Because it has no alternative.

Pharma is approaching a patent cliff that will strip exclusivity from an estimated $340 billion of annual revenue by 2030—several times larger than the last major patent cliff. The most exposed companies, including Merck and Bristol Myers Squibb, each have more than 50% of product revenue at risk from the loss of exclusivity on one or two megablockbusters[iii].

What this reveals is how concentrated many large pharma companies have become—and how dependent they are on external innovation. In 2025, roughly 70% of FDA-approved drugs had at some point been discovered or developed by a small biotech, consistent with IQVIA's 2022 finding that emerging biopharma companies account for 65% of the molecules in the R&D pipeline. The industry's R&D engine has effectively been outsourced to small caps.

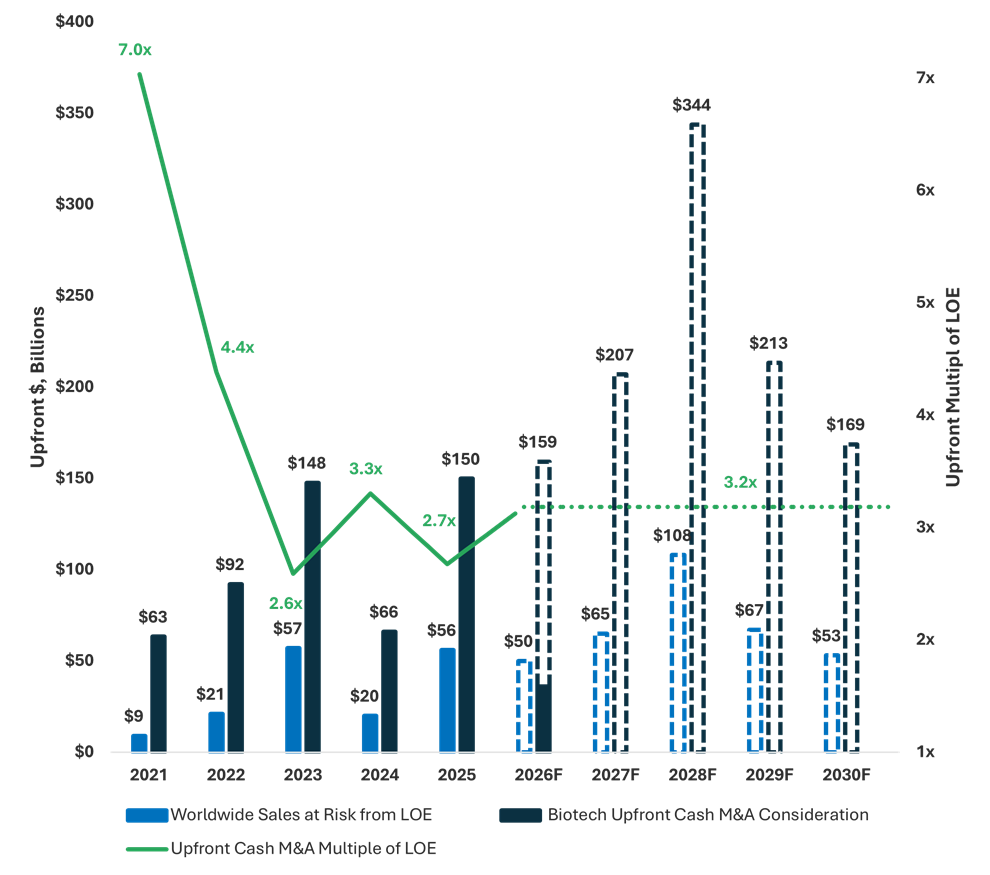

The only way to fill a hole this large on this timetable is to buy the cow or license the milk. Assuming biotech forward-revenue multiples remain broadly in line with the past five years, and pharma maintains a similar mix of M&A, licensing, and internal R&D spending, more than $1 trillion of pharma capital will flow into biotech over the next four and a half years (Figure 2).

That is forced, non-discretionary, de-risked demand aimed at a shrinking universe of shares.

Figure 2: Pharma's ~$340B loss-of-exclusivity (LOE) wave through 2030 implies $1T+ of cash outlay to replenish pipelines

Source: BCIQ & FactSet, as of June 23, 2026; Pharma Licensing of the Future, Ernst & Young, 2024; Portfolio tactics to scale the $300bn patent cliff, Evaluate, 2025; Ascendant BioCapital Analysis

Hold that trillion next to the number everyone is talking about breathlessly. McKinsey pegs data-center CapEx at $6.7 trillion by 2030, $5.2 trillion of it for AI—about six times the outlay that pharma could spend on biotech M&A by 2030, and by McKinsey's own admission resting on unclear demand, unproven ROI, and inference costs it calls a major unpredictable variable.

No one can say a priori how many tokens a task will burn or which tasks AI will take over. Biotech's bet is the boring inverse: a B2B business with one customer, pharma, that must buy. Its central question, "does the molecule work?," is binary but answerable, and the answer is priced in incrementally as stage-gated clinical milestones occur. It's not quite the same scale as AI CapEx, but still within one log and much more certain. The market treats biotech as junk and AI as quality, even going so far as to extend investment-grade credit ratings that are predicated on structuring away speculative AI demand, while assigning distressed valuations to an entire sector selling into existential demand.

Own the index and you are already long the $5.2 trillion bet on the hyperscalers, the new mega-listings, and the crowded top of the tape, whether you underwrote it or not. The uncorrelated leg most portfolios systematically underweight isn't exotic, just specialized. It is the counterweight to the increasingly correlated index at roughly one-sixth the size of the CapEx boom: structural demand forced to bid by branded products losing exclusivity. By contrast, the market's demand for fresh dollars, which year-to-date are being channeled almost exclusively to AI, is largely assuming that "if you build it, they will come" at any price. You don't have to love biotech to appreciate the downside skew from holding too much concentration on one side of the market and not enough on the other.

Beware the Tide Going Out

Follow that $5.2 trillion to the balance sheet. The megacap US equity bull case rested on out-earning everyone while buying back stock and shrinking float—the very profile the net-issuance factor rewards. That is changing.

Apollo's Torsten Slok notes the Mag 7's earnings edge over the S&P 493 converging and hyperscaler free cash flow rollover as CapEx climbs. The decade-low P/E premium looking less like cheapness than the market catching up to the eroding quality of the earnings beneath it. When CapEx eats cash flow, the buyback goes first. Meanwhile, the supply of public shares is growing. SpaceX has delivered the largest listing in history into nearly every index fund; Alphabet, long the archetypal buyback machine, sold roughly $85 billion of equity to finance its AI ambitions; SK Hynix is floated about $28 billion of ADRs on Nasdaq; and Anthropic has filed for a late-2026 listing, with OpenAI potentially slipping to 2027. This does not even consider other potential public issuance by some of the largest private companies, including Anduril, Stripe, Discord, Canva, Redvolut and Databricks queued behind the initial wave of big hecto- and kilocorns and megacap follow on offerings.

In the first quarter of 2026, net issuance for US nonfinancial corporates turned positive for the first time in over a decade (Table 1)—while biotech keeps retiring during the good times and the bad times. Biotech continued to shrink its float in the very quarter the "quality" began flooding the zone with paper, a trend that has and will continue to accelerate.

Friends Don't Let Friends

So—is biotech junk? On one metric that is predictive of returns, the net supply of stock, it behaves like the opposite, whatever the models and the dinner-party consensus insist. As I wrote last month: the best bets can come dressed like junk.

None of which makes biotech easy. Biotech investing is still capital intensive, still binary, still able to take your head off. However, the structural bid, pharma's forced buying into a shrinking float, is a fact about the sector. Getting your head taken off by a single name, underwritten wrong or just being caught on the wrong side of a wide confidence interval, is an accident that can largely be mitigated through disciplined underwriting and diversification. A strong breeze is filling the sector's sails; the capsizings belong to individual boats that took a bad tack or sailed under a poor skipper. The role of the allocator has never been to pick the one molecule that works, but to own the structural return while sizing and diversifying away the binary risk that ends careers. That gap is the whole reason active biotech exists.

Friends don't let friends buy single-name biotech alone: back an experienced manager, own the XBI for the factor, or stay away with a clear conscience. There are many talented biotech managers out there, including several in my own peer cohort who are just setting out, with strong incentives to perform and AUMs still small enough not to crowd out the best opportunities for returns. Any of them could be a partner for decades, if and when you decide the sector is worth your time. Just don't hate biotech for the one thing it doesn't do.

A trillion-dollar bazooka of forced, de-risked buying is aimed at the shrinking float of biotech; five trillion of hopeful, unproven CapEx is aimed at inflating everyone else's float. I'll let you decide which one is the junk.