Lions' Mouths and Free Lunches:

Finding Structural Alpha in Biotech's Existential Gambles.

Image: ChatGPT, Ascendant BioCapital

Image: ChatGPT, Ascendant BioCapital

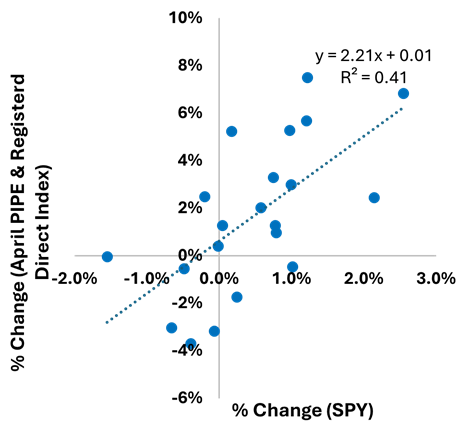

Biotech PIPEs (private investments in public equity) and registered direct equity offerings may seem like risky transactions for investors. If you were to construct a deal‑weighted index of April PIPE and registered direct issuers, the profile is exactly what you'd expect: average pre‑deal market caps of $681M, accumulated deficits of $483M, and TTM net losses of $81M (Table 1), combined with daily price moves about 2.2x those of the S&P 500 and a sizable idiosyncratic return component (Figure 1).

Table 1: Biotech PIPE and Registered Direct Financings Conducted in April

|

Pricing Date |

Company |

Deal Type |

Deal Value ($M) |

Pre-Financing Market Cap ($M) |

Number of Investors[i] |

Accumulated Deficit ($M)[ii] |

Net Loss ($M)[iii] |

Performance to Present (May 11, 2026) |

|

|

4/30/2026 |

Valneva SE |

PIPE |

$43.3 |

$473.1 |

8 |

$662.4 |

$135.3 |

34.9% |

|

|

4/29/2026 |

GH Research plc. |

RD |

$117.5 |

$1,231.3 |

3+ |

$154.4 |

$47.6 |

18.1% |

|

|

4/28/2026 |

Climb Bio Inc. |

PIPE |

$110.1 |

$453.8 |

11+ |

$289.7 |

$59.9 |

17.1% |

|

|

4/27/2026 |

Sagimet Biosciences Inc. |

RD |

$175.0 |

$190.9 |

9+ |

$346.3 |

$51.9 |

28.2% |

|

|

4/21/2026 |

Maze Therapeutics Inc. |

RD |

$150.2 |

$1,334.2 |

8+ |

$489.5 |

$131.1 |

8.6% |

|

|

4/20/2026 |

Prelude Therapeutics Inc. |

RD |

$90.0 |

$366.5 |

2+ |

$683.1 |

$99.5 |

8.1% |

|

|

4/16/2026 |

Adlai Nortye Ltd |

PIPE |

$150.0 |

$530.0 |

14+ |

$464.8 |

$35.3 |

-2.2% |

|

|

4/16/2026 |

MeiraGTx Holdings plc. |

RD |

$100.0 |

$916.3 |

ND |

$816.2 |

$114.2 |

10.0% |

|

|

4/13/2026 |

ImageneBio Inc. |

PIPE |

$30.0 |

$54.8 |

4+ |

$230.1 |

$45.3 |

7.9% |

|

|

4/13/2026 |

Sana Biotechnology Inc. |

PIPE |

$25.0 |

$824.6 |

1 |

$1,839.0 |

$244.2 |

6.9% |

|

|

Weighted Average |

$99.1 |

$681.4 |

$482.9 |

$80.7 |

13.7% |

||||

Source: Company press releases, SEC filings, Yahoo Finance, Ascendant BioCapital Analysis

Figure 1: April Daily Returns of PIPE and Registered Direct Index vs. SPY

Source: Yahoo Finance, Ascendant BioCapital Analysis

The Cruelest Month?

April was a blistering month for equities. The S&P 500 rallied 10.5% on strong corporate earnings, prospects of resolution of the war with Iran and the normalization of transit through the Straits of Hormuz.

Unsurprisingly, during April this hypothetical deal-weighted index of ten biotech companies generated 40.1% returns (Figure 2): seemingly an open and shut case of market timing and catching a risk-on environment at the right time. But there is something much more nuanced and structural driving this performance and excess return.

Probably Not Recommended by Your Financial Advisor

Prudent investors categorically avoid investments in companies whose values could fluctuate wildly based on global macroeconomic events. Even more so when it's intrinsically difficult to hedge out macro & market exposures in these investments.

This is especially the case in a market environment where the engines of growth over the past five years appear to be stalling. Paul Tudor Jones recently expressed the view that tech "has dogged it andwill continue to dog it" due to increasing hyperscaler CAPEX and the widely anticipated new share listings of a select group of hectocorns and kilocorns. This will eat into Tech's FCF and fuel net share issuance for the first time in over ten years, respectively. The concern around the $3+ trillion[iv] private credit industry's stress is equally alarming. When a fund like BlackRock TCP Capital Corp. discloses a 5% markdown on NAV, what does that imply about the markdowns at the portfolio level? Is it concentrated—such as a handful of investments experiencing severe or total losses—or is it diffuse, with more modest markdowns spread across the entire portfolio? Both scenarios produce the same headline 5% decline, but they carry very different implications for risk, correlation, and future losses. Which is more troubling? At one extreme, the fund faces catastrophic defaults in limited holdings without any recovery, most certainly suggesting some correlation given the coincidence of large losses and therefore more catastrophic losses on the come. On the other extreme, a universal markdown of 5% implies either exceptionally bad underwriting standards, ubiquitous deterioration in debt service, or both. Private credit has become essential financing supporting over three-quarters of the $4+ trillion[v] private equity buyout fund ecosystem. So, what is an investor to do to achieve a multiple on their capital within 5-7 years?

With storm clouds building on the horizon for markets, and small-cap biotech appearing both risky and highly correlated to US equities, why should investors lean into this opportunity set of publicly traded small-cap biotech companies with significant financing needs and no near-term prospects for commercialization?

Birmingham Screwdrivers

Unlike most investors, this is familiar territory for me. I've spent nearly two decades across public biotech, venture investing, and discovery‑stage operations—alongside partners whose experience, collectively, spans many decades in the space. For me, the reason to focus on small biotech companies' equity is simple: this is the toolset I know best.

While biotech public equities and venture capital are generally treated as distinct investment universes, their risk characteristics overlap considerably. In practice, many VC funds carry significant public NAV, reflecting the view among managers that an IPO is typically not an "exit event," but rather a "financing event." Public markets facilitate clearer price discovery around key development milestones that underpin VCs' underwriting assumptions and, ultimately, inform downstream M&A outcomes. Furthermore, the universe of small- and mid-cap biotech companies is largely comprised of companies that are still years away from a commercial product and are currently conducting some of the same types of clinical studies that private biotech companies conduct. Yes—publics tend to be more advanced in development. But for the most part the dividing line is that one universe is marked-to-market daily and has the ability to trade and the other does not.

So why go from privates to publics? And why, specifically, focus on small-caps that are limited to raising capital in financings perceived as being highly risky?

The Alpha, but Not the Omega

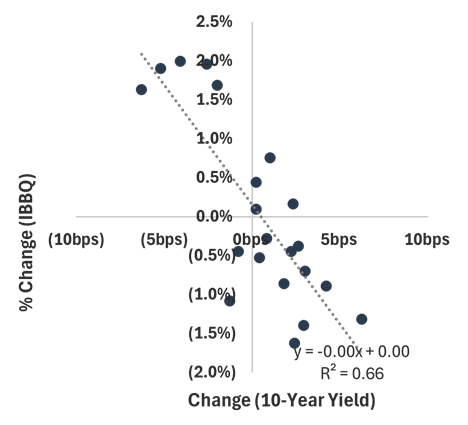

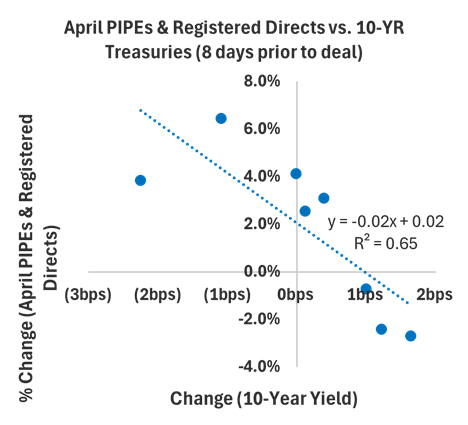

As an R&D heavy industry with lengthy development cycles, access to capital is the lifeblood of biotech—especially for small-caps relying on PIPE and registered direct financings. But the data present an interesting paradox. In April, changes in the daily 10-year Treasury yield explained two-thirds of IBBQ's daily returns (Figure2). That sensitivity is much less pronounced among companies that completed PIPEs and registered directs during the month, explaining only half of the daily price moves (data not shown). This is counterintuitive: IBBQ is dominated by profitable biotechs like Vertex, Gilead, and Amgen, along with well‑funded large‑caps that need little near‑term financing and enjoy strong capital markets access, while the PIPE cohort still faces years of capital needs and far less predictable access to equity funding. Rates may dominate short‑term price moves, but biotech is valued over time on events—clinical progress, financing outcomes, and M&A prospects—and resolving an existential financing cliff is one of the most predictable events for markets to reprice.

Figure 2: Biotech is Highly Rate-Sensitive in the Short-Term, but Paradoxically Less so for Small-Cap Companies That Finance

|

|

|

Source: Yahoo Finance, CNBC, Ascendant BioCapital Analysis

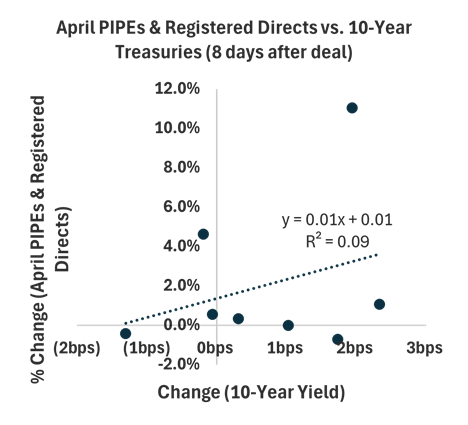

Borrowed Time

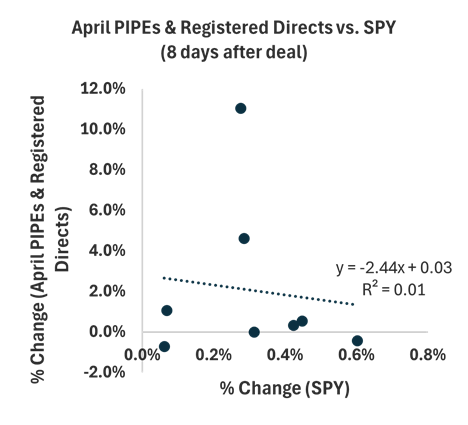

A key reason this small-cap cohort is less sensitive to interest rates comes down to resolving the existential concern of running out of cash before critical value-inflecting data can be generated. Once that pressure is relieved, managements can execute more effectively, morale and productivity improve across teams, and the next phase of development can get underway. Just as financial deleveraging can generate structural alpha, paying back the time borrowed by operating with an empty gas tank can do the same. The data bear this out: when indexed to the dates of their April PIPE or registered direct financings, this cohort of companies shifts from being highly levered to both the S&P 500 and interest rates to largely indifferent to both (Figure 3). Importantly, this shift isn't static—rate sensitivity and beta tend to build heading into a financing, compress sharply once the deal clears, and then gradually re‑emerge as cash balances are spent down, creating a tactical setup around the timing of capital raises.

Figure 3: Biotech Financing Serves as a Structural Deleveraging Event

|

|

|

|

|

|

Source: Yahoo Finance, CNBC, Ascendant BioCapital

Heads in Lions' Mouths

Much like a circus ringmaster sticking his head in a lion's mouth, small‑cap biotechs are at the mercy of the equity capital markets to decide whether their projects have enough merit to advance to the next stage of development. That dynamic gives clubby PIPE and registered direct investor syndicates meaningful leverage in pricing financings. These deals are often done on an over‑the‑wall basis, giving buyers an information advantage, and post‑financing ownership tends to remain concentrated in relatively few hands with limited public float. Together, these factors can lead to selective persistence in outsized performance when catalysts work favorably for investors.

Free Lunches

Why should investors love small‑cap public biotechs in this market? Maybe it's the growth potential, as these companies sit at the earliest stages of clinical development—where the most meaningful information about efficacy, safety, and commercial viability is first revealed. Maybe it's the benefit to human health, since investigational therapies have the potential to tackle some of medicine's most intractable challenges.

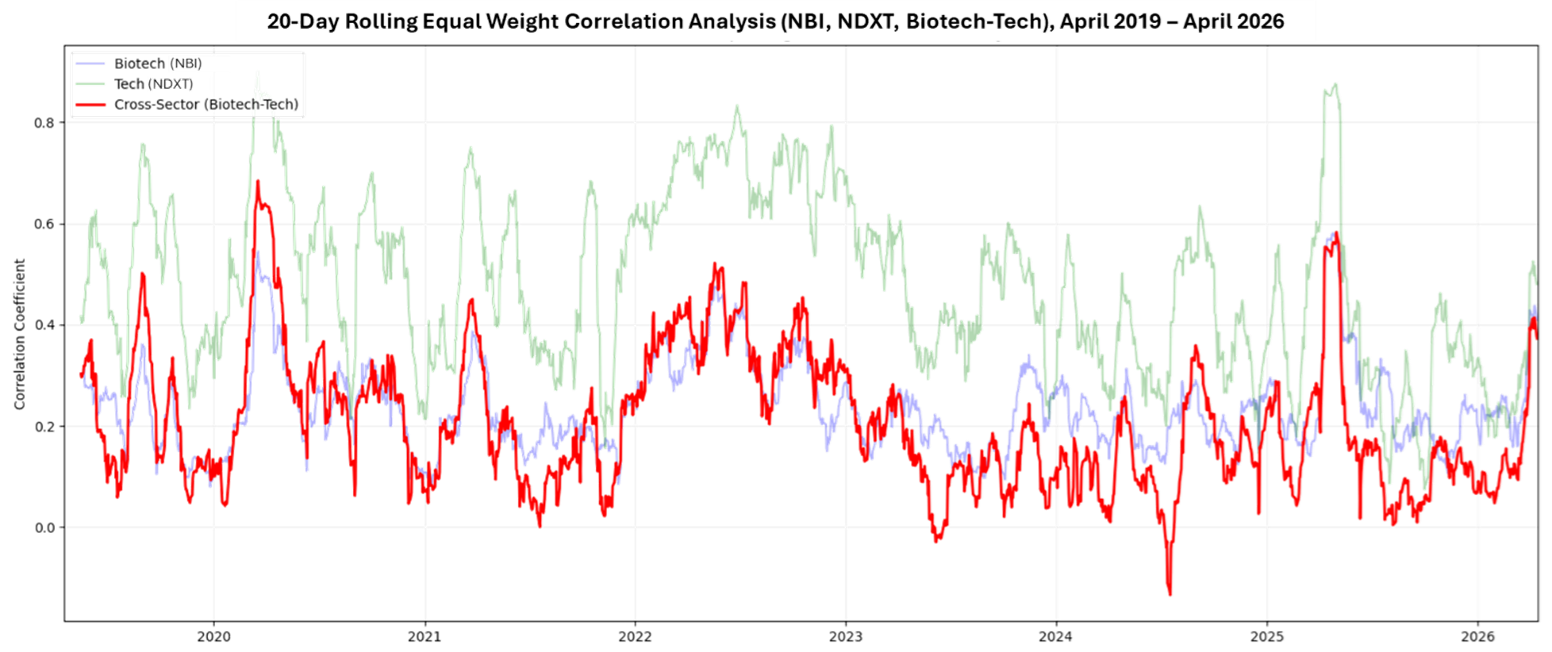

The most compelling benefit is the portfolio diversification impact. Specifically, strong returns and low correlations that look more like alternatives, but with public‑market liquidity (Figure 4), driven by independent events—data readouts, regulatory decisions, financings, and transactions—rather than corporate earnings alone. Taken together, small‑cap biotech offers something increasingly rare in today's markets: long‑duration growth, real‑world impact, and a return profile that doesn't have to move in lockstep with everything else—the free lunch of diversification, with the feast being the chance to find the next Vertex or Regeneron still trading in the clearance aisle.

Figure 4: Biotech is Largely Uncorrelated (Biotech Stocks vs. Other Biotech Stocks, and Biotech vs. Tech)

Source: Yahoo Finance, Ascendant BioCapital Analysis (data as of April 15, 2026)