Beware Greeks Bearing Gifts:

The greatest threats can seem like risk-free gifts, and the best bets can seem like junk.

Image: imgflip.com, Ascendant BioCapital

On June 4th, with the VIX closing at a sleepy 15.40, I attended a symposium where a panel on "investing in resilience" sparked a surprisingly high level of investor engagement.

The focus was on sectors that are insulated from today's seemingly compounding chaos: water infrastructure; near-shored production immune to deglobalization and the cycles of executive flippancy that only judicial and market guardrails keep in check; technologies built to defend against asymmetric warfare, where a rogue state can threaten the Strait of Hormuz with a $1,500 mine or a $20,000 Shahed drone, defying America's 126-to-1 military spending advantage; and businesses shielded from technological disruption now moving faster than anyone can update their DCFs.

2026 started with a bang, and "resilience" may well be the allocator buzzword of the year. The search has started for assets whose fate isn't hostage to headlines. Diversification is dead. PIMCO declares that geopolitical risk is "a feature rather than a bug", while Morgan Stanley warns that stocks and bonds increasingly fall together, killing the traditional 60/40 portfolio. Compounding the issue, Apollo's Chief Economist points out that new financing across all asset classes this year is heavily biased toward a single factor risk: AI.

Investors want assets that provide idiosyncratic returns, and if those assets also provide the increasingly scarce, baseline necessities of Maslow's pyramid, even better.

The Asymmetric Shield of Biology

Biotech is a strange and overlooked candidate for a macro resilience strategy. A company developing an investigational medicine does not care whether the Strait of Hormuz is open or if a Louisiana data center gets built. Its value depends on whether a molecule works inside the human body. For pre-commercial assets, valuation is driven by the reduction of technical and regulatory risk that occur throughout clinical development. A tariff can tax an eventual product, but it cannot alter clinical probability of success any more than the Fed's interest rate policy can influence biology. AI can model clinical probabilities, but it cannot prove them. Unlike SaaS, where software can be disrupted overnight by AI-generated code, biotech remains moored to clinical endpoints proven through empiricism across a diverse and chaotic sample of human biology in clinical trials.

Investing in biotech provides something humanity will always demand: better care when our health fails or death comes knocking on our door. It also creates systemic resilience by shifting societal spending from chronic to prevented interventions, just as statins have structurally reduced revascularization procedures and ICU stays at scale. The pace of innovation over these past three months alone points to an inflection occurring in biotech:

- A first-in-class KRAS G12D inhibitor controlled disease in nearly 80% of heavily pretreated pancreatic cancer patients.

- A PD-1VEGF bispecific cut the risk of death by 34% in squamous lung cancer.

- GLP-1s fundamentally altered obesity prevalence while driving secondary health outcomes, like preventing breast cancer in women.

- A gene therapy provided functional cures for a rare genetic disease in most patients.

The China Dilemma: Bounty vs. Dependency

However, true resilience is not just about delivering idiosyncratic returns that are uncorrelated with the broader market but requires planning for a world of deep geopolitical friction. In biotech, the center of gravity for discovery and early development is rapidly shifting east. Chinese biotechs now run preclinical and early proof-of-concept trials faster and cheaper than their Western counterparts.

Global pharma has noticed. China-originated assets made up roughly a third of global out-licensing deal value in 2025, up from single digits four years ago, an edge analysts expect to persist. By 2030, I estimate that more than 30% of the US biotech and pharma pipeline will originate from Chinese biotechs.

This shift exposes the reality that biotechnology is now a critical strategic industry. It presents as a classic Trojan horse: a bounty of cheap, fast molecules that no licensee wants to refuse, wheeled through our gates with strategic dependence riding inside.

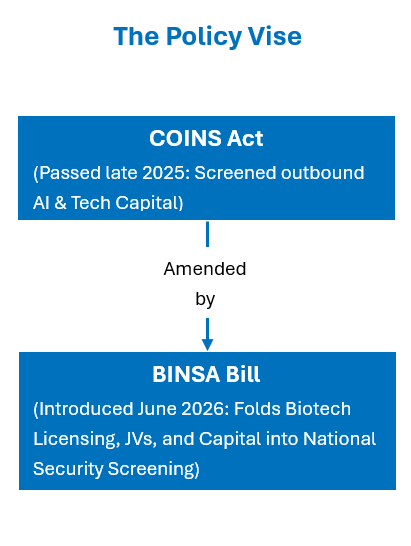

This risk is no longer hypothetical. The policy response is rapidly erecting a vise to stem this tide:

|

|

This political squeeze is happening exactly as domestic science absorbs proposed cuts to the NIH, threatening the foundational research the private sector rarely funds, and potentially costing American patients.

For investors and America, more broadly, navigating this landscape requires a dual-track strategy:

- The Imperative for US Domestic Biotech Investment: Cultivating independent sovereign capacity is non-negotiable. The capacity to discover, manufacture, and field countermeasures domestically is national resilience in its most literal form. We are seeing this play out in real time: the Ebola outbreak now spreading through the DRC and Uganda is a Bundibugyo strain for which no approved vaccine or treatment exists. If underfunding and geopolitical separation hollow out our domestic research infrastructure, we lose our shield against emergent or engineered pathogens.

- Arbitraging the East-West Yield: Simultaneously, smart capital must recognize that we cannot simply blind ourselves to global innovation. The arbitrage opportunity for Western investors lies in in-licensing and structural insulation. By in-licensing early-stage Chinese molecules, American companies can leverage an outsourced discovery engine to benefit US patients, while capturing the downstream commercial profits to fund and sustain independent domestic research.

The goal should not be total isolation, but strategic control. We can capture the benefits of global science while reinforcing an unassailable domestic foundation, avoiding a retreat into an autarkic world order.

The Gift Left Outside the Gates

If biotech is a cornerstone of a macro resilience strategy, the pressing question is: how does one invest when development cycles are lengthy, technical failure is high, and massive follow-on capital needs are almost certain?

One compelling option is what I call the "institutional reverse merger," a private company—often recently formed through a spinout of a compelling clinical asset—going public via a shell, paired with a concurrent private investment in public equity (PIPE) to fund its operations. These transactions mimic venture capital exposures, typically targeting preclinical to Phase 2 assets with median pre-money valuations of around $185 million. Like venture financing, these deals are syndicated among biotech specialist institutional investors, fund the companies' operations directly, and provide cash runway through the proof-of-concept experiments that provide the sharpest de-risking of a clinical program.

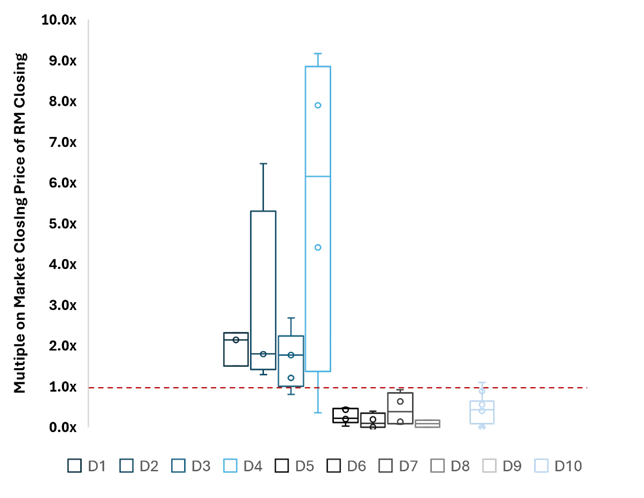

Historical data on forty-one reverse mergers that have closed since 2023 reveal a stark relationship between capital and performance. Companies that raise concurrent PIPEs greater than $65M see their share prices rise 87.5% (14/16) of the time after the transaction closes, whereas those that raise $65M or less can expect to face significant losses in share price, 96% (24/25) of the time (Figure 1).

Figure 1: Reverse merger PIPEs below $65M (≥5th decile) destroy value; those above $65M generate robust, low loss-rate returns.

Source: Ascendant BioCapital Analysis, Capital IQ (courtesy of LifeSci Capital)

Why does a PIPE of $65M determine which cohort is successful and which is almost exclusively failures? It just happened that there was a neat, observable cut point between the 4th and 5th deciles in the amount of capital raised in concurrent PIPE financings. Post-hoc, this makes some intuitive sense to me. Companies need sufficient runway to complete the next phase of development, and then additional runway to pursue a transaction or raise follow-on capital after clinical milestones reset valuation. It is hard to think of a clinical-stage public company whose operating cash needs for two years or more are $65M or less. The requirement to repeatedly generate enough new investor demand also serves as a useful sorting function, filtering for the programs that can sustain conviction from fresh capital over time.

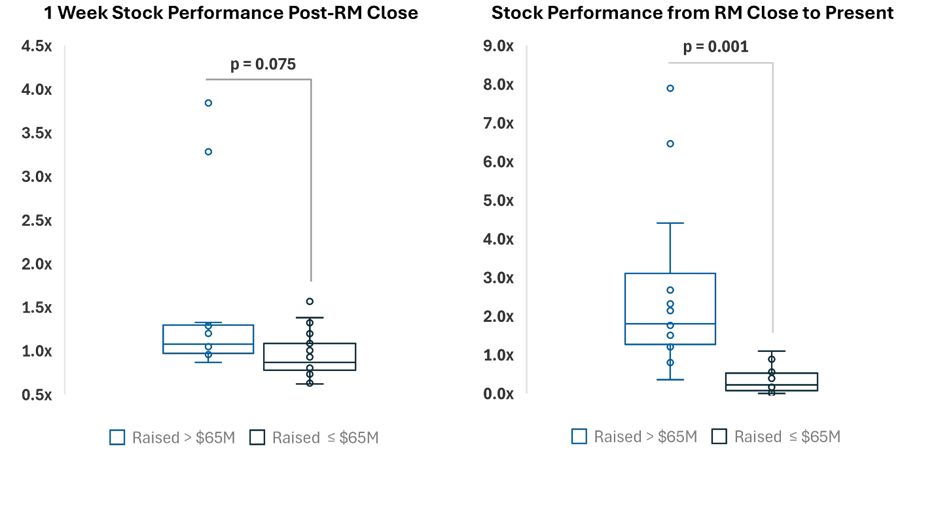

The numbers are tough to argue with. Across this "institutional reverse merger" cohort, the average return from the closing date through late May 2026 was 2.96x (2.45x when weighted by the PIPE financing size), with a median return of 1.80x.

Figure 2: Post-merger performance split by $65M PIPE threshold. The long-term, but not short-term performance gap is highly significant (p = 0.001).

Source: Ascendant BioCapital Analysis,

Capital IQ (courtesy of LifeSci Capital)

Source: Ascendant BioCapital Analysis,

Capital IQ (courtesy of LifeSci Capital)

For perspective, Cambridge Associates' data puts the top 5% of 2023-vintage healthcare venture funds at a TVPI of 1.4x (2024 and later vintages are still too immature to count). In other words, the median institutional reverse merger has comfortably outperformed the best-in-class private healthcare funds. And it did so while marking to market daily, providing real-time price discovery, and giving management cheaper, more certain access to follow-on capital.

Oral Gavage for the Citadel of Indexing

Which brings us to the event the entire market is watching. Tomorrow, SpaceX is set to list on Nasdaq under the ticker, SPCX, at $135 per share. It is the largest IPO in history—a massive $1.75 trillion valuation floating just a tiny 4% fraction of its shares.

But public capital's appetite extends beyond rockets. Just days prior, on June 9th, Parabilis Medicines priced a $670 million debut, which represents the largest IPO ever for a venture-backed biotech, eclipsing even Moderna's 2018 record. It caps a frantic 2026 where newly public drugmakers have raised a median of nearly $300 million apiece, more than double last year's pace. The mega-listing is not unique to SpaceX and the hectocorns. They just have the imagination to do it at log orders greater scale and get to skip the queue to force everyday savers to buy in.

Yet history is notoriously unkind to IPO buyers. Decades of data from Jay Ritter show that new issues underperform size-matched firms by roughly 3.6% annually for five years, with nearly two-thirds lagging the market by year three.

Historically, index providers protected passive investors through "seasoning", which forced companies to earn their seats in indices over several quarters before inclusion. No longer. Nasdaq now fast-tracks mega-caps into the Nasdaq-100 after just fifteen days of trading, while FTSE Russell inserts them after five.

Index funds—and the retail savers behind them—will be forced to absorb an unseasoned, 4%-float colossus, triggering at least $14 billion in automatic, price-insensitive buying, in one of the greatest risk-transfers of all time. This is the horse at the gate: an irresistible brand paired with a tiny float, wheeled straight into the citadel of nearly every retirement portfolio in the country before anyone has investigated what lies inside. The Trojans, too, celebrated around their gift before midnight arrived.